Alex Shtarkman

Revolution Team

April 3, 2023

4 min

Proptech is a relatively nascent investing vertical. The first inklings of the buzzword can be traced back to 2012 but took on virality (in my view) around 2017–2018 — around the time my friend Michael Beckerman began producing CRETech, one of the leading proptech conference, research, and thought leadership organizations devoted to innovation in the built world. The last five years have been a wild ride for participants in the burgeoning category. There have been some massive, category-defining winners (like Airbnb), several monumental failures (like Katerra), and everything in between (like WeWork). All offer lessons learned — even the modest exits. This blog series is meant to serve as an unvarnished, data-driven lookback on proptech in order to debunk some of the commonly held myths and analyze key lessons learned.

Let’s start by analyzing capital inflows into proptech, the stratification of dollars across deal stages, and an overview of the investor universe from 2018 to 2022.

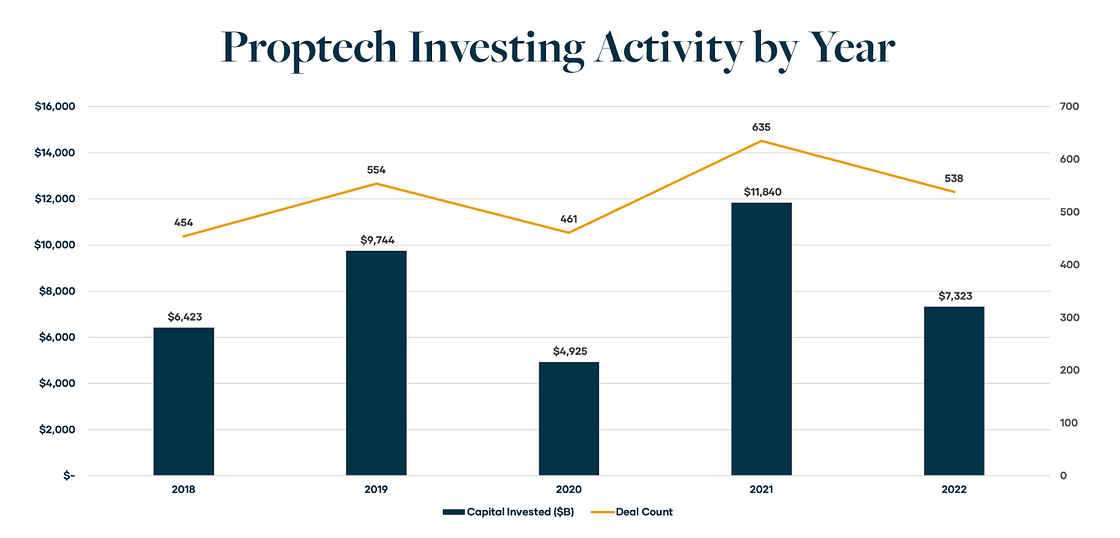

Debunking Myth #1: There has not been a single “golden” year for proptech to date. In fact, deal activity (measured in both dollars and deal count) has been quite volatile over the last five years. While more than $40B has been deployed into proptech companies across 2.6K+ deals, much of that capital has flowed to a select number of companies. Since 2018, there have been eight $500M+ financings. There have also been 28 $200M-$500M financings — that is more than $14B in capital raised by only 28 companies, or 35% of the aggregate capital invested in the last five years. Excluding these mega financings, the per-company average financing is around $10M per deal — the size of a typical Series A investment. With 1.2K+ unique proptech companies raising capital during this period, a simple average suggests roughly two financings per company. So, the category is not as liquid as it seems — the amount an “average” proptech company could expect to reasonably raise has historically been quite limiting.

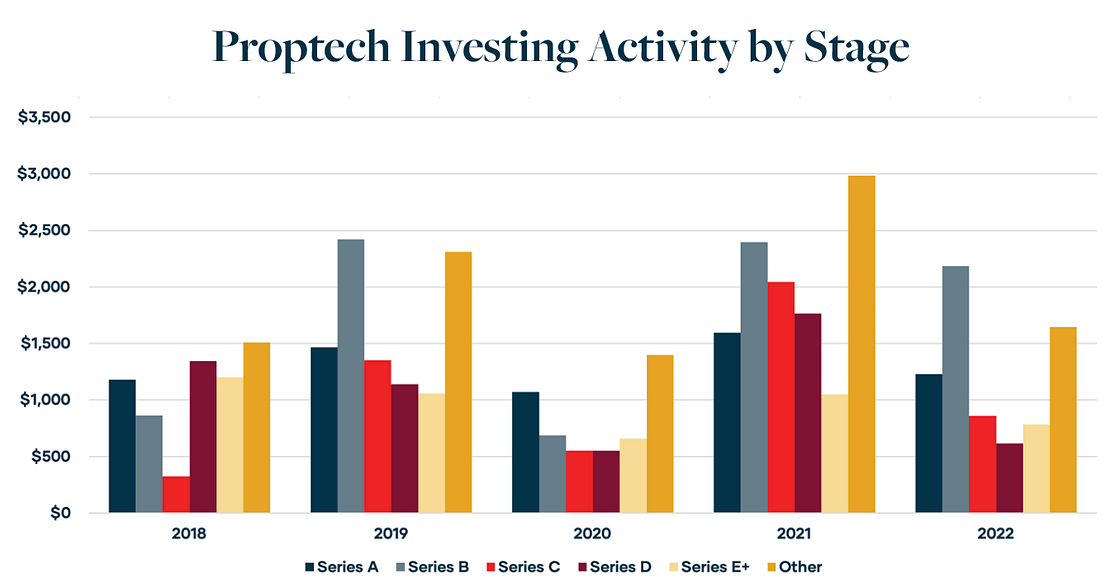

Debunking Myth #2: Capital flows have not been disproportionately concentrated in the early stage (supporting new company formation). While the data is imperfect (as a material portion of financings is unclassified by PitchBook), the investment dollars are roughly split between Series A and B financings (early-stage) and Series C+ financings (late-stage/growth-stage), as illustrated below. What does that mean? If you were a proptech company raising a Series A in the last five years, roughly half of available fundraising dollars went to later-stage companies. Said another way, of the more than $40B deployed into proptech, only approximately $20B was accessible to early-stage proptech companies.

Debunking Myth #3: VCs have not solely fueled the rise of proptech. Proptech is unique within the VC space because a proptech’s customer, investor, and likely buyer can all be the same persona: the institutional owner/operator or a large real estate strategic — making the proptech universe quite finite.

In the last five years, more than 4.3K investors have written a check into a proptech deal. An outsized number come from the real estate community: asset managers, family offices, and corporate venture capital arms. Angel investors are also extremely active in the category — anecdotally, most of these participants are real estate senior executives and professionals who have followed their firms, colleagues, and friends into venture deals. Altogether, these strategic investors account for 46 percent of the total investor universe, compared to venture capitalists’ 42 percent.

Accordingly, it’s not uncommon for a proptech’s cap table to contain more individuals or tourist investors than institutions. These strategics are oftentimes one-time check writers viewing the opportunity to invest as largely an internal R&D investment (i.e., a way to experiment with innovation inside one’s real estate portfolio), as compared with an institutional venture investor’s perspective of underwriting a deal with emphasis on generating returns upon ultimate exit. The unintended consequence is that, despite a greater pool of potential lead investors for a deal, there are fewer parties around the table interested in active company management, day-to-day governance matters, and building a sustainable business that generates lasting returns.

When a startup is growing quickly, the classification of investors on their cap table matters less as long as demand for follow-on capital investment remains a non-issue. But, when a startup hits speed bumps, the investor syndicate comes into focus — and not all capital allocators are created equal. Each has varying investment models and incentives that may or may not align with the reality of a scaling startup.

In summary, proptech is still an emerging category, and I believe the best is yet to come. With a market correction underway, now is a good time to reflect on proptech successes and failures to drive progress. Next, I’ll explore the evolution from Proptech 1.0 to Proptech 2.0, a shift I believe is already underway — stay tuned!

.svg)